The full story on funding a school fees plan

Our full team of advisers give their advice on the wealth planning areas that you need to consider

When it comes to paying for your family’s private education, “can I afford it?” is usually the first question that you ask. It should not, however, be the last. From how to pay school fees in a tax-efficient way to affording payments if your circumstances change, school fee planning is a complex topic. With tax opportunities, risks and interrelated financial issues to consider, the decisions that you make can dramatically impact your wealth.

Whether you are a parent paying for your children’s fees or a grandparent offering financial assistance, it is important to seek professional advice. Having helped hundreds of families, our team of advisers are well versed in all aspects of succession planning. Their in-depth knowledge and experience allow them to effortlessly move from determining affordability to highlighting tax planning opportunities. Discussions and reviews also help to highlight any newly ‘at risk’ areas of your existing financial strategy.

Creating a school fee plan: seeking succession planning advice

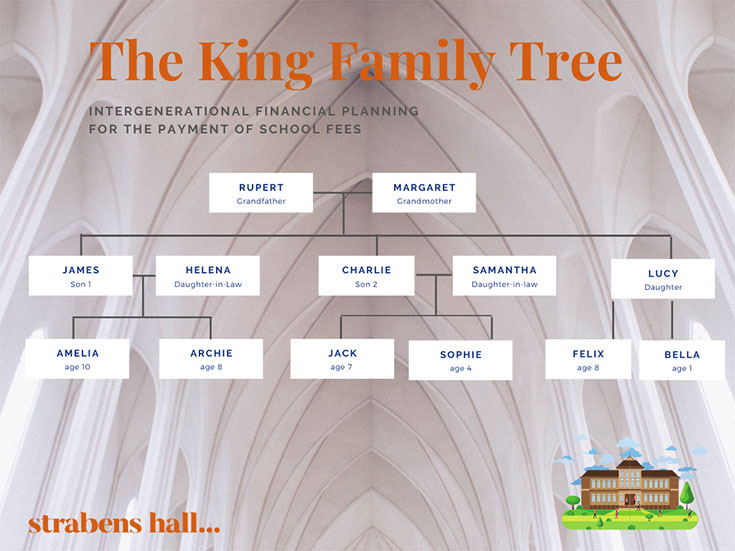

As with all financial advice, there is no ‘one size fits all’ solution when it comes to school fee planning. There are, however, a number of common scenarios that many families face. These scenarios have inspired the creation of our King family case study.

Over the summer, we shared the Kings’ school fee planning journey on our LinkedIn and Twitter pages. Rupert and Margaret – our clients – have decided that they want to pay half of their grandchildren’s school fees. However, while James and Charlie’s children are – or will be – enrolled in a private school, Lucy’s eldest child, Felix, attends a state school.

As such, the couple have come to us seeking answers to the following questions:

- How much can we afford to give our grandchildren each year?

- Should we switch to more income generative investments?

- How should we fund school fees payments?

Cash flow planning: can the Kings afford to pay for their grandchildren’s private education?

Before we – or the Kings – can take the next step, we first need to find out whether or not they can afford school fee payments. Linda Kozlowska, our Senior Client Director, runs cash flow planning exercises to find out.

These exercises highlight the fact that, yes, the couple can afford to help pay for their grandchildren’s school fees. Each year, they are able to give away up to £103,000. Based on their cash flow report, the couple can continue to do this, while maintaining their current lifestyle, until they are 100 years of age. Additional money – for a holiday or an unexpected expense – is also available to them annually.

The impact of school fee planning on the King’s investment strategy

While the cash flow report confirms the fact that Rupert and Margaret are in a strong financial position, it raises some interesting questions about their investment portfolio. Our Senior Client Director, Nicholas Toubkin, discusses the appropriate level of risk that they need to take in order to achieve their financial goals. He also notes that their “existing investment portfolio is exclusively invested into direct securities and fixed income holdings, with a strong bias towards UK-based assets.” While this offers them protection from currency fluctuations and reduces ongoing management costs, it also means that their portfolio might be lacking in diversity.

An in-depth conversation about the couple’s broader goals for their wealth allowed us to uncover Rupert’s concern for environmental issues. This, in turn, means that Rupert and Margaret can be made aware of opportunities in environmental, social and governance (ESG) funds.

In response to their question, “should we switch to more income generative investments?”, Nick points out that their portfolio is intended to be income generative. While this strategy has worked well to date, he suggests regular review to ensure that “the current strategy remains appropriate” given the impact of Covid-19 on corporate earnings and dividends.

School fees and tax planning: trusts and inheritance tax

For Rupert and Margaret, there are tax advantages to funding their grandchildren’s private school fees. Christopher Yardley, our Client Director, provides us with more detail.

“Rupert and Margaret can each utilise their annual gift allowance of £3,000 a year. This reduces the value of their estate subject to Inheritance Tax (IHT) and is considered an ‘exempt transfer’.”

The couple have asked him whether it is worth setting up a trust fund for their grandchildren’s school fees. He notes that there are a number of “tax-planning structures available, including bare trusts, discretionary trusts and family investment companies.” If the couple gift into one of these structures, “the amount of IHT payable on the gift tapers down from year three to year seven.” After seven years, the gift will no longer be considered as part of the estate for IHT purposes; they are, therefore, seen as potentially exempt transfers (PET).

A substantial new expense: the need for a family risk audit

While the focus here is on Margaret and Rupert, the continued ability of Charlie and Jack to pay for half of their children’s school fees must be assessed.

“A family risk audit is an exercise to help identify any shortfalls and frame the agenda for an informed discussion as to what actions, if any, they may need to consider to bridge gaps,” our Executive Director, John Halley says.

The family risk audit uncovers the following facts:

- Charlie has a life insurance policy through his current employment. He and Samantha also have a joint-life, first death, life and critical illness policy.

- Jack’s current employer provides him with a subsidised – and relatively generous – sick pay policy. This policy enables him to receive payments through to retirement age should he become ill or be unable to work due to an accident.

- If something were to happen to Charlie’s wife Samantha, Charlie may find himself having to pay potentially significant childcare costs, which would reduce as the children get older.

To protect against potential financial difficulty caused if Samantha was to pass away, John was able to recommend a decreasing term ‘family income’ insurance policy.

From the family risk audit, we can now see that Jack and Charlie are both financially secure enough to meet their financial commitments. However, John recommends that “their position should be reviewed on a regular basis, and on any change of employment.”

Pension Planning – Using pension income to fund school fees

John Moore, Client Director at Strabens Hall, turns his attention to Rupert’s pensions. He discovers that:

- Rupert receives £50,000 per annum from his Defined Benefit scheme. The income that this provides increases each year, but it is taxable. If he passes away before Margaret, she will continue to receive 50% of his pension. Rupert’s age must be taken into consideration before making any recommendations. If he dies on or after his 75th birthday (he is currently 74 years of age), Margaret will be able to withdraw funds from his Defined Benefit scheme, but at her marginal rate of tax (as opposed to it being free from tax if he dies before he turns 75).

- Rupert also has a Self-Invested Personal Pension (SIPP) worth approximately £900,000. It is uncrystallised, meaning that he has yet to draw any benefits from it.

John tells us, “the SIPP is a useful asset to pass down the generations to children or grandchildren and therefore withdrawing benefits from Defined Contribution pension last, where possible, is recommended.” He also makes the point that, if it is passed on, the SIPP “would normally be outside of the estate for the calculation of IHT.”

As can be seen from the conclusions drawn by John, when considering pensions as part of your succession plan, it is important to ensure that the holder’s age and the rules associated with pensions are taken into consideration.

How to be tax efficient when paying school fees

Next, our CEO, Adam Benskin, looks at the ways in which the couple can fund their grandchildren’s school fees most tax efficiently from their various assets. These assets include surplus cash, equity release, a Family Investment Company (FIC), surplus income exemption and settling nil rate band (NRB) discretionary trusts.

Adam discusses how each could be used. Rupert and Margaret could, he tells us, “consider using surplus cash to pre-pay school fees, which is tax-efficient because the payment would be treated as PET, with the gift falling out of their estate after seven years.” Alternatively, “gifts from surplus income are immediately exempt from IHT, subject to meeting the qualifying criteria.”

He continues, suggesting that “equity release could be considered towards funding a PET” if necessary or that “the grandchildren could be issued shares in the FIC.” Moreover, “surplus cash and ISAs [could be used] to settle NRB discretionary trusts, without triggering capital gains tax.”

While there are a number of options available to the couple, Adam reminds us that this advice is not the same for everyone; it is always important to seek personalised advice and to ensure that, over the years, the advice originally given remains viable.

The legal risks associated with school fee planning

Once affordability has been determined and interrelated financial matters have been reviewed and discussed, it is important to consider any legal ramifications. Will Ford, Partner at global legal firm, Womble Bond Dickinson, states that while “every family setup is different”, there are key risks that can impact all families.

If you are giving a gift, make sure that there is “no debate about whether funds have been given away or lent,” he tells us in our Successful Succession Planning podcast. “The law doesn’t help if you didn’t write it down.”

Will recommends communicating clearly and honestly – be it, for example, through letters or family meetings. The importance of doing so grows further if family members have been treated differently.

Succession planning and structuring a school fee plan

Here at Strabens Hall, we know that every client, every family and every situation is unique. When you come to us for financial advice, we start with an open mind and a blank sheet of paper. We warmly welcome your family and your other professional advisers into our discussions to help you preserve and structure your wealth intelligently.

To discuss succession planning, structuring a school fee plan or any of the other matters highlighted here, contact us at our Soho or Nice office.

Strabens Hall Ltd is authorised and regulated by the Financial Conduct Authority (“FCA”). Our FCA registration details are set out in the FCA Register under firm reference number 461795 (www.fca.org.uk). Strabens Hall Ltd is registered in England and Wales (registered number 06015275) and our registered office is 5 – 9 Eden Street, Kingston upon Thames, Surrey, United Kingdom, KT1 1BQ.

Some of our services are not regulated by the FCA. Before you engage us in any work, we will outline which of those services are and are not regulated by the FCA to enable you to make a fully informed decision.

The Financial Ombudsman Service (FOS) is an agency for arbitrating on unresolved complaints between regulated firms and their clients. All complaints for referral should be submitted to Strabens Hall Ltd prior to approaching the Financial Ombudsman Service (FOS). Full details can be found on its website at www.financial-ombudsman.org.uk.